HCA Healthcare previewed its second quarter this morning, and on the surface it reads fine. Revenue of $20.23 billion, up from $18.61 billion a year ago. Net income of $1.699 billion, or $7.62 a share. Adjusted EBITDA of $4.03 billion. CEO Sam Hazen said his colleagues "continue to manage well through the positive and negative factors that have impacted our business in the first half of the year."

The interesting number isn't in the quarter. It's in the guidance.

Source: HCA Healthcare Q2 2026 preliminary results, July 14, 2026

The line that matters

HCA took a $400 million unfavorable pre-tax hit in Q2 from a shift toward uninsured patients, "primarily due to health insurance exchange coverage losses," plus another $75 million truing up Q1's estimate.

Then they moved the full-year assumption. The 2026 exchange impact went from ($600M–$900M) to ($1.0B–$1.2B). That range didn't drift. It roughly doubled at the midpoint, halfway through the year.

This is the enhanced premium tax credit expiration showing up in a hospital P&L, on schedule and in cash. When the subsidy goes away, the marginal enrollee drops coverage first: younger, healthier, price-sensitive, and the least likely to think they need it. HCA is the other end of that trade. Those people didn't stop existing. They stopped being insured.

And they still show up. Look at the volume mix:

- Same-facility admissions +2.5%, equivalent admissions +2.7%

- Emergency room visits +3.6%

- Inpatient surgeries −2.3%, outpatient surgeries −3.4%

Demand is up, but the profitable, scheduled stuff is down while ED traffic is up. That is the signature of a payer-mix problem, not a demand problem. Elective surgery is what insured people schedule. The ED is where uninsured people go.

About that Medicaid offset

HCA booked roughly $400 million of incremental net benefit from Medicaid Supplemental Payment Programs, mostly Florida's state-directed payment program, and that figure covers October 2024 through June 2026. It's a catch-up true-up spanning almost two years, landing in one quarter, and it very nearly cancels out the $400M uninsured hit.

Don't let it. Full-year guidance flipped that assumption from ($50M–$250M) to a +$300M–$500M benefit, a ~$600M swing in HCA's favor that is doing real work propping up the year. Strip it out and the underlying story is uglier than the headline. Net income guidance still got cut to $6.30B–$6.70B from $6.495B–$7.035B, and EPS to $28.70–$30.50. Meanwhile capex guidance held at $5.0B–$5.5B. They are not slowing down.

So where is HCA, actually?

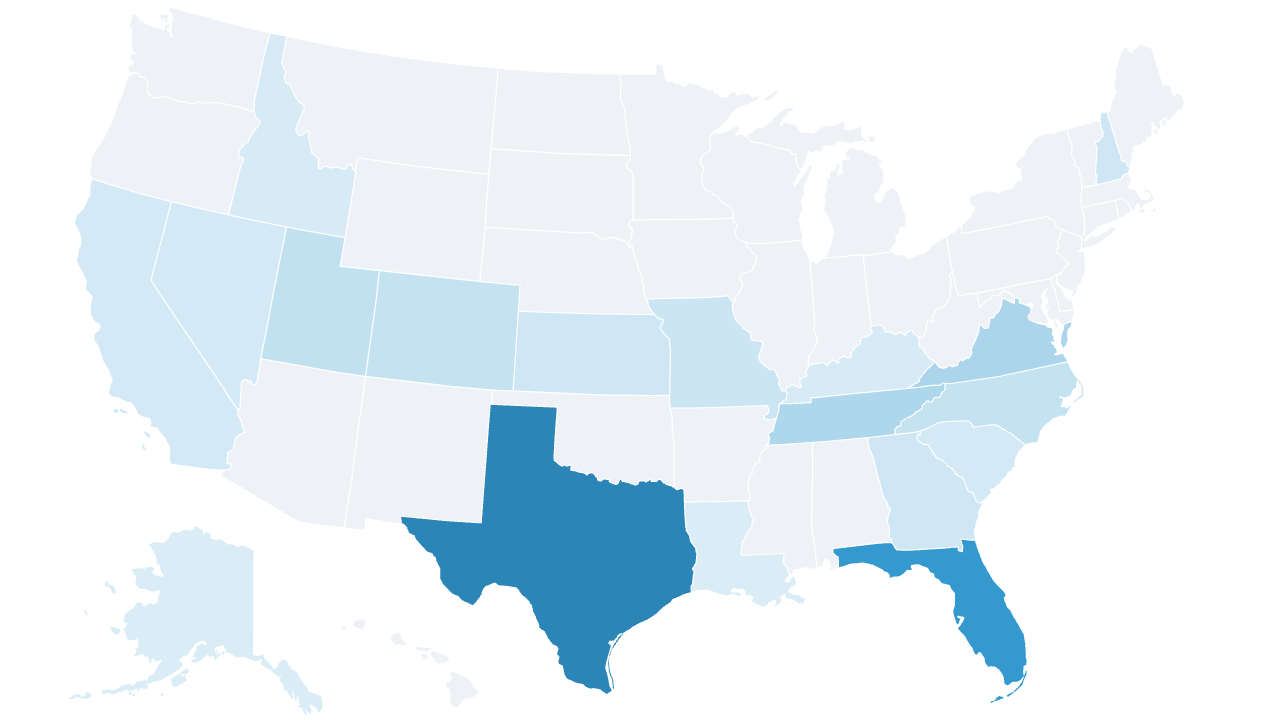

I pulled HCA's own care-location feed, the data behind the facility finder on their site, and geocoded every hospital to a county. 185 hospitals, 18 states, 106 counties.

It is not a national footprint. It's a Sun Belt footprint with a Texas problem attached:

- Texas: 56 hospitals. Florida: 48. Together that's 56% of every HCA hospital in the country.

- Tennessee (13) and Virginia (14) are the only other double-digit states.

- Seven states have three or fewer.

Now overlay the exchanges. Texas and Florida are also two of the largest ACA marketplaces in the country, and Florida is the single most subsidy-dependent state in the program. HCA's hospital concentration and its exchange exposure are the same map. That's not a coincidence. It's why the guidance moved.

The obvious conclusion is wrong

The reflex here is to say HCA has leverage, so HCA raises rates and the carriers eat it. I started there. I think the leverage half is wrong, and that's the half everything else rests on.

That reflex comes from the employer market, where breadth sells. An HR director will not buy a plan that's missing the big system in town, so the big system in town gets paid. Fine. But the ACA individual market is the one place that logic inverts, because HMO and EPO plans are already 72% of the exchange. HMOs are up 60% since 2014 and EPOs have tripled. Narrow networks don't merely survive on the exchange. They won it.

That happened because the ACA shopper does not behave like an HR director. They sort by price, look at the first two or three results, and buy. Network breadth is a tiebreaker at best. With enhanced subsidies gone, the people left shopping are the ones paying the most real money out of pocket, which makes them more price-sensitive, not less. Every dollar HCA adds to a carrier's unit cost goes straight into that carrier's premium and pushes it down the list on HealthCare.gov.

So a carrier facing an HCA rate demand has a live option: build the network without them.

Can carriers actually route around HCA?

In the markets that matter, mostly yes. That's the part the leverage story misses.

HCA is concentrated in big Sun Belt metros, and big metros have other hospitals. Houston, Dallas, Fort Worth, Miami and Tampa all have multiple competing systems with real brands and real beds. A carrier in any of those cities can assemble a network a shopper will recognize and never sign HCA. Those are also the counties with the most carriers competing, which means the most players with a reason to try.

Where HCA genuinely is the only option, it tends to be a small county with one hospital and two carriers on the exchange. That's real market power over a small number of lives. It is not what moves a billion dollar number.

The interesting middle is a place like San Antonio, where HCA has enough density to be hard to skip and there are still plenty of carriers fighting for enrollment. If HCA pushes anywhere, it pushes there. But that's the exception, and one metro doesn't fix the P&L.

So the threat "pay us more or we walk" is weaker than it sounds in exactly the places where HCA has the most to lose.

What HCA should do

Here's the thing I keep coming back to. HCA's problem is not that insured patients underpay. It's that uninsured patients pay approximately nothing. An uninsured ED visit collects cents on the dollar and lands in bad debt. That reframes the whole negotiation, because HCA's alternative to a bad rate isn't a good rate. It's a zero.

Take the same person who dropped their silver plan when the subsidy went away and put them back on a narrow-network HMO that pays HCA even mediocre commercial rates. HCA goes from collecting nothing to collecting something, on volume it is already treating anyway. That math doesn't argue for a rate increase. It argues for the opposite trade.

The case for making that trade:

- Take a lower rate to buy exclusivity. Where HCA is dense enough to be a credible network by itself, it can anchor a narrow product: the carrier gets a cheap network and a premium that ranks first on HealthCare.gov, HCA gets steered volume and converts uncompensated care into paid care. San Antonio is the obvious candidate. So is Nashville, where HCA is deeply established in its own hometown.

- Density stops being pricing power and becomes product capability. A stack of hospitals in Houston won't make anyone pay more, but it's enough to be the whole network for a Houston HMO. That's the asset here. It's worth more rented cheap than held out for a rate.

- The volume question answers itself. Can HCA walk away from ACA volume in Texas and Florida, where 56% of its hospitals sit? No. It has $5 billion of capex it isn't cutting and beds it needs filled with paying patients. You don't fund that by shrinking your covered population.

But that is not what HCA does

Here's where I have to argue against myself, because I don't think any of that is going to happen.

HCA is not the system that discounts. It runs one of the most expensive commercial books in the country, it negotiates hard, and it has spent decades making itself expensive on purpose. Deep discounting to chase exchange lives is not in the muscle memory. The playbook that built this company says you hold the line on rate and you make the carrier blink.

So the likely path is the boring one. HCA pushes rate into renewals. In the markets where it's concentrated it probably gets some. In the big metros where there are other systems to buy, it mostly doesn't, and it keeps eating uncompensated care from the same patients it would have been paid to treat.

I'd like to be wrong about that. But betting on HCA to discount its way out of this means betting against how it has done business for a very long time. Protecting the rate card is a strange way to solve a problem that isn't really about rates.

The uncomfortable version of all this: the subsidy cliff was sold as a federal savings measure. It didn't delete the cost, it moved it. It comes back as uncompensated care on a hospital's books, and it gets worked out between a system and a carrier in a negotiation nobody gets to see, over people who no longer have a card in their wallet.

Hospital locations come from HCA's own published facility feed, geocoded to counties. Worth noting: HCA's website still claims "190 hospitals in 19 states," but that map is dated June 30, 2024. Its live feed now yields 185 licensed hospitals in 18 states, and it correctly reflects divestitures the marketing copy hasn't caught up with, like West Hills (sold to UCLA Health) and Regional Medical Center of San Jose.